The System (v1): How I’m Paying Down $74,000 Without Starting Over

In my previous post, I shared why I started this. This is how the system actually works.

I have a $74,000 HELOC balance.

It’s variable rate. It’s been used multiple times over the years. And if I’m being honest, there hasn’t been a clear system behind how I’ve managed it—just a mix of paying it down, using it again, and repeating the cycle.

So instead of trying to “fix” the balance directly, I’m building a system around it.

This is version 1.

The Goal

Not to eliminate the HELOC forever.

The goal is to:

- Pay it down intentionally

- Use it more strategically

- Eventually refinance it into a new HELOC with better structure

I don’t want to remove the tool—I want to stop using it randomly.

The System (v1)

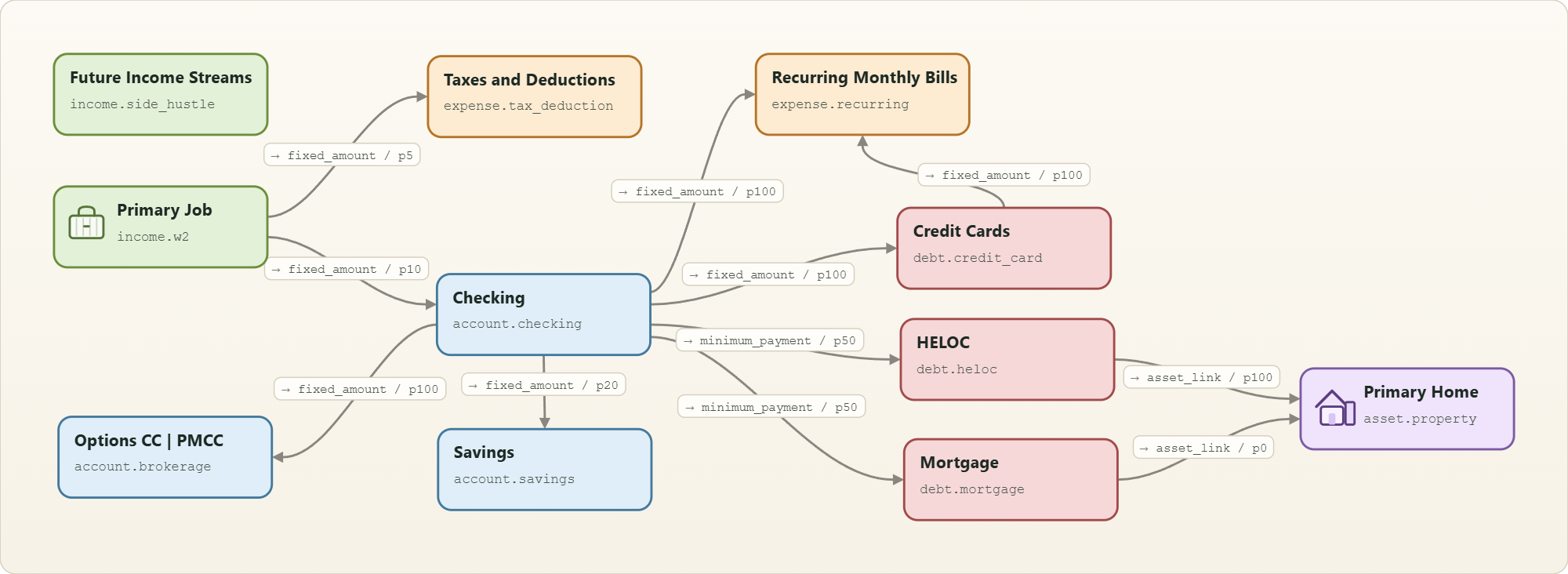

Here’s what my current setup looks like:

At a high level, everything flows through a central checking account, with defined paths to expenses, savings, and debt.

What matters isn’t just where the money goes—but how consistently it moves through the system.

1. Cash Flow Engine

Everything starts here.

Income comes in from my primary job (and eventually future income streams), flows into checking, and then gets distributed based on predefined rules:

- Fixed allocations to taxes and recurring expenses

- Payments to debt (minimums first)

- Transfers to savings

- Additional principal payments when there’s surplus

The goal isn’t to optimize every dollar—it’s to remove randomness.

Once the flow is stable, the next constraint becomes timing.

2. Credit Card Layer (Timing + Structure)

Credit cards solve the timing problem.

I use multiple cards with different due dates to manage how expenses flow through the month. Most recurring and day-to-day expenses are charged to credit cards first, then paid off from checking.

This creates two advantages:

- Timing flexibility:

I get paid bi-weekly, but some expenses—like property taxes or larger bills—don’t line up cleanly. Credit cards act as a buffer so I don’t have to time cash perfectly. - Controlled outflow:

Instead of money leaving checking constantly, spending gets grouped and paid at specific times.

All cards are paid off in full every month. This is not a system for carrying credit card debt—it’s strictly for cash flow management.

Points and travel rewards are a side effect of this setup, not the goal.

With timing handled, the next step is deciding what should run automatically and what shouldn’t.

3. Automation Layer

Not everything in the system needs attention.

The predictable parts are automated:

- Most recurring monthly bills are automatically paid via credit cards

- Utility bills (gas, water, electric) are automatically paid from checking

- The HELOC minimum payment is automatically paid from checking

Everything else stays manual.

This split is intentional:

- Automation handles what doesn’t change

- Manual payments keep me engaged with what does

With the foundation, timing, and automation in place, the remaining decisions are about allocation.

4. Income Layer (Experimental)

This is where I’m building future capacity.

I’m currently running covered calls and PMCC strategies, but I’m not using that income to pay down the HELOC yet.

A reasonable question is:

Why not use that money now to pay down the HELOC faster?

Right now, the account is still relatively small. At this size, the income it generates doesn’t meaningfully move the HELOC balance.

If I divert that income too early:

- It slows down the growth of the account

- It limits future income potential

- It turns the strategy into short-term relief instead of a long-term tool

So the plan is simple:

- Grow the account to $50K

- Let it stabilize

- Then decide how it integrates into the system

For now, it stays separate.

A similar question comes up around spending.

Why Not Just Reduce Spending?

Why not just cut expenses and use that to pay down the HELOC faster?

That would help—but it’s not the main problem I’m trying to solve.

What I didn’t have before wasn’t just lower spending—it was structure:

- How money flows

- When payments happen

- How debt gets used and paid down

Without that, even reduced spending can still lead to the same cycle.

I’m also not building this with the goal of minimizing everything.

I still want to:

- Travel

- Go out to dinner

- Maintain and gradually improve my lifestyle

So instead of shrinking expenses to fit the system, I’m building a system that can support those decisions more intentionally.

Over time, both should improve:

- Better spending decisions

- Better cash flow structure

But the system comes first.

That same thinking applies to how I approach the HELOC itself.

5. HELOC Strategy (Core)

This is the part I’ve never clearly defined before.

The plan is:

- Pay down the current balance

- Improve how I use the credit line

- Eventually refinance into a new HELOC with a fresh draw period and higher limit

So this isn’t a “debt-free journey.”

It’s about turning the HELOC into something structured and repeatable.

6. Asset Layer (Parallel Track)

At the same time, I’m building additional income streams.

Right now, that includes:

- Small tools and apps

- Content (this site included)

This is still early, which is why it shows up as “future income streams” in the system.

Over time, this layer should feed back into the rest of the system.

Rules (v1)

To keep this from drifting back into guesswork:

- No new HELOC draws without a defined purpose

- No using options income until the account reaches $50K

- Credit cards are used for timing—not for carrying long-term debt

- All credit cards are paid off in full every month

- Extra payments come from actual surplus, not forced transfers

- Everything gets tracked and shared publicly

These rules will evolve, but this is the starting point.

What This Is Not

This isn’t a guide.

It’s not optimized.

And it’s definitely not advice.

I’m building this in real time because I didn’t have a system before—and I want one now.

What Comes Next

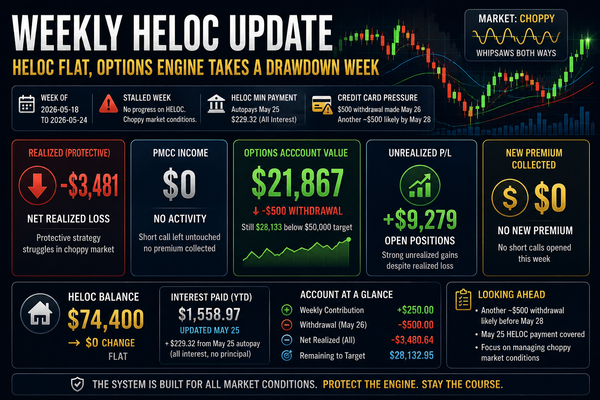

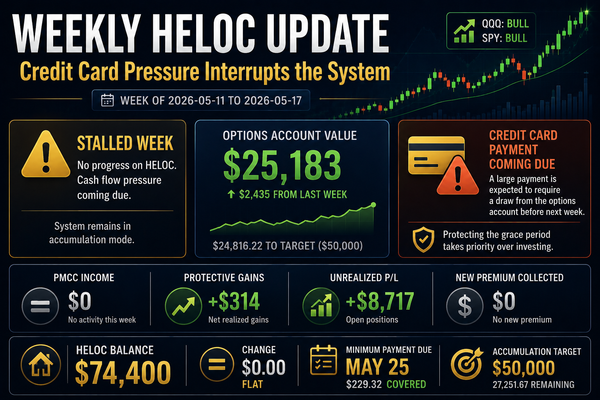

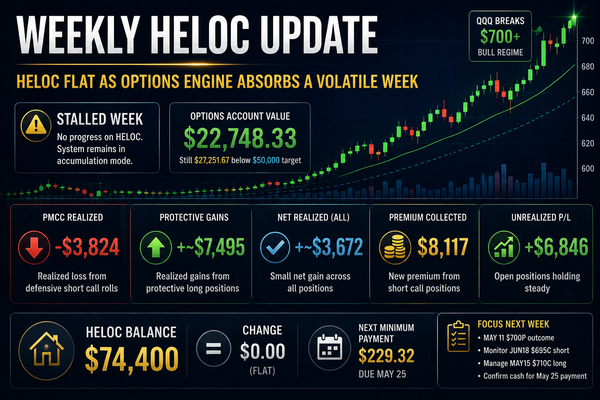

Starting next month, I’ll be posting weekly updates using a fixed template.

That will include:

- Current balance

- Payments made

- Interest impact

- Cash flow movement through the system

- Any changes to the system

The goal is to make the process visible and consistent.

This is version 1.

I’ll adjust it as I go.