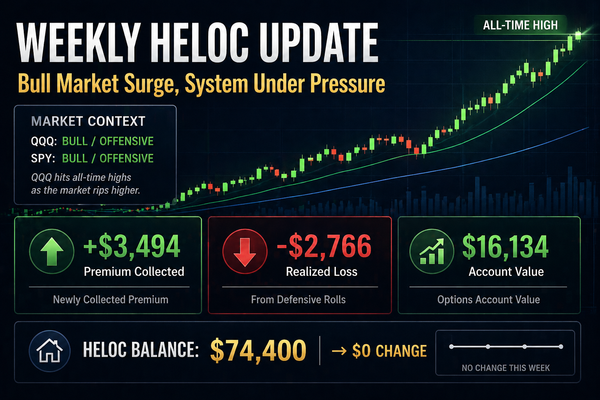

Weekly HELOC Update: Balance Flat as Protective Strategy Offsets Short Call Rolling Losses

For the week of 2026-04-27 through 2026-05-03, the HELOC remained flat at $74,400. Supporting system activity came from the option account, which finished at $17,237.46, posted realized PMCC income of -$1,001.42 from a defensive short call roll, and collected $3,801.25 in new premium. Protective long call positions generated $3,255.79 in realized gains, more than offsetting the PMCC loss. Unrealized gains held at $5,116.91.

🔗 System Context

If you're new here, this update is part of a larger system:

- How I Pay Down a $74,000 HELOC (Week by Week) — detailed weekly process

- How I'm Paying Down a $74,000 HELOC — the overall strategy

- The System (v1): How I'm Paying Down $74,000 Without Starting Over — how the system operates

- Baseline: Where Everything Stands Today — current numbers and starting point

📅 Reporting Window

- Publication date: 2026-05-04

- Week covered: 2026-04-27 through 2026-05-03

🧭 System Status

- 🛡️ Defensive Week

- A Defensive Week means the HELOC did not move, but the system executed conscious strategic decisions to maintain position stability and avoid larger losses.

- Unlike last week's Stalled classification (where defensive rolling resulted in net realized losses), this week's protective long call strategy generated enough realized gains to more than offset the PMCC rolling losses.

- The option account remains below target, so the system is still in accumulation mode.

📊 Mission Scoreboard

- HELOC balance change: → $0.00

- HELOC ending balance: $74,400.00

- HELOC interest paid (YTD): $1,329.65

- Options account value: $17,237.46

- Target level: $50,000.00

- Remaining to target: $32,762.54

- Realized option income (PMCC): ↓ -$1,001.42

- Realized gains (protective longs): ↑ $3,255.79

- Net realized income (all positions): ↑ $2,265.81

- Newly collected premium: ↑ $3,801.25

- Open-position P/L (unrealized): ↑ $5,116.91

🏠 HELOC Progress

- The HELOC stayed flat this week at $74,400.

- The option account is still in accumulation mode, so even positive realized income would stay in the system rather than go to the HELOC yet.

- PMCC strategy posted a -$1,001.42 realized loss from defensive rolling, offset by +$3,255.79 in realized gains from protective long calls (not tracked in PMCC metrics). Net realized income across all positions: +$2,265.81.

- Interest paid this week: $0.00 (first minimum payment due May 25)

- Interest paid YTD: $1,329.65 (cumulative from the original HELOC, serving as the baseline for the new line going forward)

📈 Options Subsystem Summary

- Newly collected premium: $3,801.25

- Realized option income (PMCC): -$1,001.42

- Realized gains (protective longs): $3,255.79

- Net realized income (all positions): $2,265.81

- Options account value: $17,237.46, still $32,762.54 below the current target.

- Weekly contribution: $250.00

- Dividend income: $11.44

- Open-position P/L (unrealized): $5,116.91

- LEAP holdings: ~$4,369.33 (estimated)

- Short call position: -$951.75 (1x MAY 08 $630 call)

- Protective long calls (3x MAY 04 $674): $1,743.98

What Happened This Week

QQQ remained in a strong bullish regime, continuing the all-time high momentum from the previous week. The ITM short call position required defensive management to avoid assignment.

April 27: The three protective long calls from the previous week (APR 28 $653 strikes) were closed at a profit and rolled up to MAY 01 $664 strikes. Realized gain: $1,279.89.

April 30: The ITM short call (MAY 01 $620 strike) was bought back at $48.02 and rolled up $10 to the MAY 08 $630 strike for $38.02. This defensive roll collected $3,801.25 in new premium but resulted in a realized loss of -$1,001.42 as the buy-back cost exceeded the original premium collected.

May 1: The protective long calls (MAY 01 $664 strikes) were closed at a profit and rolled up again to MAY 04 $674 strikes. Realized gain: $1,975.90.

Net result for the week:

- PMCC rolling loss: -$1,001.42

- Protective long call gains: +$3,255.79

- Total net realized income: +$2,265.81

The protective long call strategy—buying ATM calls to hedge against the ITM short call exposure—continued to prove effective in this bullish regime. The protective positions captured gains on the same upward movement that put pressure on the short calls, resulting in net positive execution for the week despite the PMCC rolling loss.

This strategy may be formalized as a standard rule for managing PMCC positions during sustained bullish market regimes.

🌍 Market Context

- QQQ: BULL / offensive

- SPY: BULL / offensive

QQQ's continued bullish momentum required ongoing defensive management of the ITM short call position. The protective long call strategy served its purpose—offsetting the cost of rolling the shorts while maintaining exposure to further upside. The system absorbed the rolling loss through the protective hedge, demonstrating that the defensive adjustments from the previous week are working as intended.

The unrealized P/L held steady at $5,116.91 despite the account value increasing from $16,134.99 to $17,237.46. The account growth came from realized gains on protective positions, the weekly $250 contribution, and dividend income.

🔍 Next-Week Watch Items

- Watch whether the newly collected $3,801.25 in premium (MAY 08 $630 short call) converts to realized gains or requires further defensive rolling.

- Monitor the three protective long calls (MAY 04 $674 strikes) as they approach expiration—these may be rolled again or closed depending on market movement.

- Track whether QQQ's bullish regime continues or shows signs of consolidation, which would reduce pressure on the ITM short call.

- First HELOC minimum payment due May 25—confirmation of automated payment setup should happen before then.