How I Pay Down a $74,000 HELOC (Week by Week)

A real-world HELOC paydown system built for bi-weekly income, uneven cash flow, and long-term consistency.

New here? This post walks through how the system runs week-to-week. For context on the strategy and results, start with the strategy or how the system works.

Introduction — Why This System Exists

This is the system I use to manage and pay down a $74,000 HELOC on a weekly basis.

At ~7% interest, that's about:

- $439 per month

- Over $5,000 per year

And it's not fixed. The rate is adjustable, which means it can go down — but it can also go higher. If the rate moves to 8.5%, that's roughly $525 per month — an extra $1,000 per year in interest with no change in behavior. That cost shows up whether progress is being made or not.

If nothing changes, the HELOC doesn't go away. It just continues to drain cash in the background.

"Why not just throw extra money at it?"

I've tried that approach before — random, reactive extra payments whenever cash feels available. It never sticks. It always turns into a timing problem:

- income comes in bi-weekly

- expenses don't line up cleanly

And there's always something competing for that cash — known obligations like the mortgage, insurance, and property taxes; unexpected hits like replacing an AC condenser in the middle of summer; and lifestyle choices, like the cruises I genuinely enjoy.

The system isn't built for a version of life without those things. It's built for life with them.

That doesn't mean extra principal payments can't happen. It means they need to be structured — recurring, sustainable, and built into the weekly process rather than depending on willpower or perfect cash flow timing. The system is designed to support that kind of consistency once the rhythm is established.

That includes planned home renovations. The balance on this HELOC is going to go up before it comes down. Phase 1 — replacement windows, stucco, siding, and exterior paint — is planned for late summer. The costs aren't fully priced out yet. That's part of the honest picture. The HELOC isn't just a debt to eliminate. It's a tool — and using it for improvements that add value to the property is a legitimate use of that tool. What the system controls isn't whether draws happen. It's what happens after they do.

So those extra payments become inconsistent, reactive, and easy to skip. And when that happens, progress stalls. The real problem isn't the math. It's consistency — because cash flow isn't perfectly timed, and real life doesn't pause just because interest is accruing.

So instead of relying on timing or willpower, I built a system.

The goal is simple: turn inconsistent cash flow into consistent HELOC paydown.

Everything else — the weekly process, the classifications, the options account — is built to support that one objective.

If you have bi-weekly income, uneven expenses, and a balance that never seems to move — this is the system I built for that.

The Weekly Cycle

Income is consistent — I get paid bi-weekly. But cash availability isn't. Some weeks have excess cash. Some weeks are tight. Some weeks are negative. Because of that timing mismatch, the system can't rely on perfect moments to act. Instead, it runs on a fixed weekly cycle.

Every week follows the same structure:

- Observe the cash position

- Confirm obligations are covered

- Run the HELOC layer

- Run the options engine

- Layer in additional income

- Classify the week

Nothing is skipped. Nothing is optimized week-to-week. The structure stays the same regardless of what the market or cash flow looks like.

Instead of asking "is this a good week to pay extra?" the system answers "what does the process say to do this week?"

Step 1 — Observe the Cash Position

Every week starts with one question: what does the cash situation actually look like right now?

The answer comes from Quicken. Every Sunday — or as close to it as the week allows — transactions are downloaded across all active accounts: checking, credit cards, and the HELOC. Not just checking. The full picture.

The Sunday review is a habit in progress, not a perfected ritual. Sometimes it happens mid-week instead. The goal is consistency, not perfection — which is true of the system as a whole.

From Raw Balance to Available Cash

The checking balance is the starting point, not the answer.

Quicken's bill scheduler pulls forward last year's transaction history to project upcoming obligations — mortgage, utilities, insurance, recurring bills. It's not a perfect forecast. Credit card amounts still need to be verified against emailed statements, and some bills vary month to month. But it gives a reliable skeleton of what's coming out and when.

The process is straightforward: take the checking balance, subtract known upcoming bills within the next 30 days, and what's left is what the system can actually work with. Not what's in the account — what's available after obligations are accounted for.

That number drives every decision that follows.

The Credit Card Layer

Most expenses run through credit cards — not because of a spending problem, but because of a timing advantage. Charging an expense delays the cash outflow by days or weeks, which smooths the gap between bi-weekly income and uneven expenses.

A $1,200 property tax bill charged on the 3rd doesn't pull cash from checking until the statement closes and the payment clears — potentially 3 to 4 weeks later. That float is real, and the system uses it deliberately.

Two rules make this work:

- Statement balances are always paid in full — credit cards are timing tools, not debt

- If a card is carrying a balance at a higher rate than the HELOC, that gets prioritized before any extra goes to principal

Credit card due dates are tracked through Quicken's bill scheduler. Statement amounts are verified against emailed statements before payment. Nothing is assumed.

Step 2 — Confirm Obligations Are Covered

Before anything moves toward the HELOC beyond the minimum, one condition has to be true: everything that needs to be paid is either paid or reserved.

Non-negotiables:

- Mortgage

- Utilities

- Insurance

- Credit card statement balances

- HELOC minimum payment

"Covered" means one of two things — already paid, or the cash is sitting in checking and not available for anything else. The system doesn't assume money will be there later. It only works with what's already accounted for.

This is where Steps 1 and 2 connect but don't overlap. Step 1 answers: what do I have? Step 2 answers: what's already spoken for? What remains after Step 2 is the only number that matters for the HELOC decision in Step 3.

Some weeks that remainder is meaningful. Some weeks it's close to zero. Both are valid outputs. The system doesn't need a surplus every week — it needs an honest read of what's actually there.

Step 3 — The HELOC Layer (Baseline + Opportunistic Paydown)

The HELOC has two modes. Both run every week. Only one is optional.

Baseline (Required)

The minimum payment runs every month without exception. This is non-negotiable — it keeps the account stable and the system from falling behind. Everything else determines whether the balance actually moves.

Opportunistic (Extra Principal)

Extra principal payments don't run on a schedule. They run when conditions allow. Before anything extra goes to the HELOC, three checks happen:

1. Where is the most expensive debt right now?

The HELOC isn't always the highest-priority payoff target in a given week. If a credit card is carrying a balance at a higher rate — even temporarily, like a property tax charge that hit before the statement closed — that gets addressed first. The HELOC rate is ~7%. Most credit cards run significantly higher. Paying the HELOC while carrying credit card interest would be moving in the wrong direction.

2. Are there known large expenses within the next 30 days?

If a mortgage payment, insurance bill, or other large obligation is within the window, that cash stays put. The system doesn't make extra payments and then scramble to cover known obligations.

3. Does the checking balance clear a working threshold after those are accounted for?

There's no hard floor yet — that number will get defined as the system matures. For now the question is simple: after subtracting what's coming out, is there anything left that isn't already spoken for? If all three checks pass, the extra goes to principal.

The Recurring Transfer (What This Is Building Toward)

Right now, extra payments are still largely event-driven — a bonus, a tax refund, a third paycheck month. Those windfalls have historically gotten absorbed rather than directed. That's the behavior the system is designed to replace.

The target is a consistent automated transfer from every paycheck — starting at $500 or less to make sure it's sustainable, with a planned increase around the 3-month mark once the rhythm is established. The amount isn't fixed. What's fixed is that something moves every pay period.

Draw Management (When the Balance Goes Up)

Paying down a HELOC while planning to draw on it again isn't a contradiction. It's just an honest description of how a revolving credit line works in real life.

Phase 1 renovations — replacement windows, stucco, siding, and exterior paint — are planned for late summer. The draw amount isn't fixed yet. Pricing is still being gathered. What is fixed is the principle: any new draw gets treated as a deliberate decision, not a default.

The current HELOC's draw period is approaching its end. Before Phase 1 work begins, the plan is to refinance into a new HELOC with a fresh draw period and higher limit — resetting the clock on the line's flexibility while maintaining the same paydown structure. The refinance isn't contingent on the balance being zero. It's about making sure the tool still works the way it's supposed to before the renovation draws happen.

Before a draw happens, two conditions are checked:

1. Is this Phase 1 or Phase 2?

Phase 1 projects are already categorized as necessary. They move forward when pricing and timing align. Phase 2 projects — longer-term improvements beyond the immediate scope — require a more deliberate evaluation, ideally timed to when a second income stream is contributing enough to absorb the additional minimum payment load.

2. Does the system absorb the new minimum payment without breaking?

Every draw increases the balance and, with it, the minimum payment. Before a draw is made, the question isn't just "can I afford the project?" It's "can the system carry the higher minimum without stalling?" If the answer is no, the draw timing gets adjusted — not the project.

The goal isn't to keep the balance frozen. It's to make sure every increase is intentional, the system can absorb it, and paydown resumes as soon as Phase 1 is complete.

Key Principle

The goal isn't to eliminate the HELOC as fast as possible. It's to control how it gets paid down over time — steadily enough that the process outlasts the moments when motivation doesn't.

A payment that wipes out the buffer and forces a cash advance two weeks later doesn't reduce the balance. It just moves it.

Step 4 — The Options Engine (Accumulation Mode)

The options account is a separate system running in parallel. It doesn't interact with the weekly cash flow decisions — by design.

The strategy is a poor man's covered call — long LEAPS as the underlying position, short calls sold against them to generate premium income. The premium is the target. The LEAPS are the vehicle.

Where It Stands Right Now

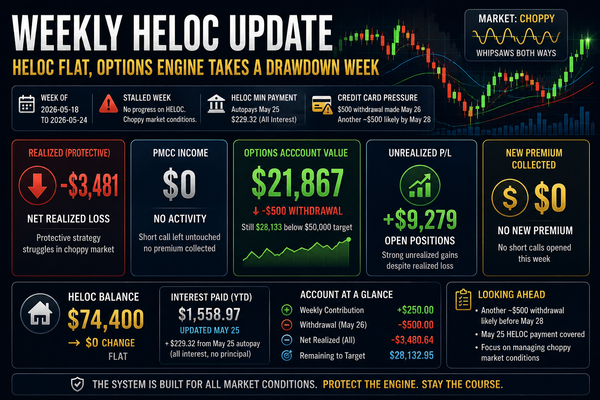

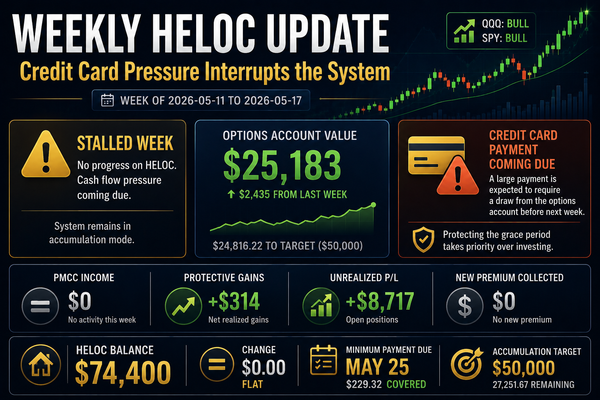

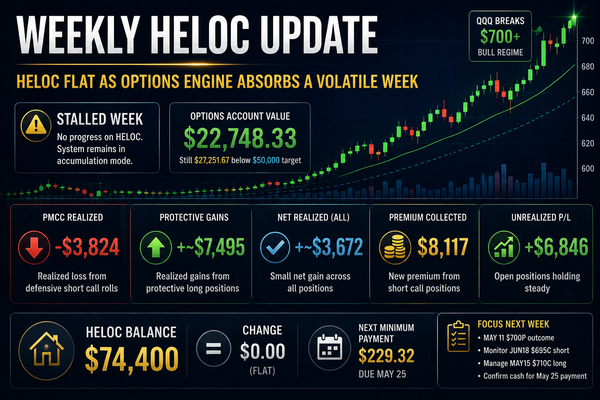

The account is currently at approximately $12,500, working toward a $50,000 threshold. It took a hit recently — broader market conditions pushed the underlying LEAPS down in value, and while the short calls were profitable, the premium didn't fully offset the decline. That's how the strategy behaves in a down market. The income is real. The path isn't linear.

The account is funded from weekly cash flow — $125 per week until now, increasing to $250 per week starting this week. At that contribution rate, plus premium reinvestment, the $50,000 target is roughly 3 to 4 years out under stable market conditions.

Why $50,000?

At $50,000, the account should generate enough monthly premium to cover the HELOC minimum payment without touching principal. That's what the threshold is based on — not a round number, but a functional one. Once the engine covers the minimum, the cash that was coming from earned income to cover that payment becomes available for principal instead.

The Tradeoff — Why Not Send $250/Week Directly to the HELOC?

It's a fair question and worth answering directly.

Sending $250 per week straight to the HELOC would reduce the balance faster in the short term. At that rate, it's roughly $13,000 per year in additional principal — meaningful progress on a $74,000 balance.

But once the HELOC is paid off, that $250 per week stops producing anything. The paydown is a one-time event.

The options account is built on a different premise: that $250 per week compounding into a premium-generating system will eventually produce more than $250 per week in income — consistently, without requiring a paycheck dollar to do it. At that point, the engine doesn't just pay down the HELOC. It outlasts it.

That's the tradeoff. Slower progress on the balance now, in exchange for a system that generates income after the balance is gone.

Phase Structure

Phase 1 — Accumulation: No withdrawals. All premium reinvested. Weekly contributions from paycheck. Account builds toward $50,000.

Phase 2 — Coverage: Premium income covers the HELOC minimum. Paycheck dollars that were covering the minimum shift to principal. The engine and the paycheck work together.

Phase 3 — Acceleration: As additional income streams come online and prove consistent, excess premium and redirected paycheck dollars stack. Principal payments increase without requiring more earned income to do it.

Step 5 — Layering In Additional Income

The options account is the first engine. It won't be the last.

The long-term vision is a system where multiple income streams contribute to HELOC paydown — so that no single source carries the full weight, and earned income from a primary job does progressively less of the heavy lifting over time.

That's the vision. The current reality is more modest. Right now, the options account is the only stream outside of primary employment that's actively running. Everything else is in early stages — digital income streams that haven't yet produced consistent results. That's worth saying plainly, because this system is built on honest accounting, not optimistic projection.

The Rule for New Income

Any new income stream has to prove itself before it gets built into the system. Proof isn't a feeling. It's consistency — the same stream producing income repeatedly, over enough cycles to establish a pattern. The threshold depends on the source. A stream that produces once isn't proven. A stream that produces reliably across multiple months starts to earn a place in the plan.

Until a stream clears that bar, it doesn't get counted on. It doesn't offset an obligation. It doesn't replace a paycheck dollar. It gets watched.

This rule exists because the system already has one vulnerability: earned income is the primary funding source for everything — the HELOC minimum, the options contributions, the mortgage, all of it. Adding an unproven stream as if it were reliable doesn't reduce that vulnerability. It just adds complexity and a new way for things to go wrong.

How New Streams Get Added

When a stream proves consistent, it gets assigned a role — in order of priority:

- Cover a fixed obligation (starting with the HELOC minimum)

- Free up a paycheck dollar that was covering that obligation

- Redirect that freed dollar to principal

The stream doesn't get spent. It gets deployed. The goal is always the same: reduce how much the primary paycheck has to do.

Each income stream will get its own dedicated post as it develops. This post sets the frame. The details will follow when there's something real to report.

Step 6 — Classify the Week

At the end of every week, the week gets a label. Not a grade. Not a judgment. Just an honest read of what happened.

✅ Progress

An extra principal payment was made — any amount. It doesn't matter if it was $50 or $500. If something beyond the minimum moved to principal, the week counts as progress. The balance is lower than it was seven days ago.

🛡️ Defensive

The minimum was paid, the buffer held, and stability was maintained — but no extra principal was made. This wasn't an accident. It was a conscious call: a known constraint made paydown the wrong move this week. The system didn't fail. It made the right decision for the conditions.

The AC condenser, the property tax charge on the credit card, the mortgage timing — these are Defensive weeks. They're built into the system, not exceptions to it.

⚠️ Stalled

The HELOC didn't move, and the week didn't produce a clear progress or recovery signal. No extra principal, no conscious defensive decision — just a week where the system didn't produce a result. An unexpected expense wiped out available cash, a timing gap left nothing after obligations hit, or the week simply fell through the cracks.

A single Stalled week is not a problem. It's acknowledged and the system moves forward.

Two or three in a row is a signal — not to change the system, but to understand what's causing the disruption. Is it a recurring timing gap? A cash flow pattern that hasn't been accounted for? A buffer that needs to be defined? The classification doesn't fix anything on its own. It makes the pattern visible before it becomes a habit.

No Overreaction

One week's classification doesn't change anything. The system isn't adjusted week-to-week based on results — it's followed week-to-week regardless of them.

What changes behavior is patterns, not moments. A Stalled week followed by a Progress week is the system working. Three Stalled weeks in a row is worth a conversation with yourself about what's actually happening.

Quarterly Review

The weekly classification handles the short view. The quarterly review handles the long one.

Every quarter the system itself gets evaluated — not the results, but the conditions: Has income changed? Have fixed obligations shifted? Is the options account on pace? Are the three payment checks still the right checks?

The goal of the quarterly review isn't to optimize. It's to confirm the system is still built for the life it's actually running in — not the one it was designed for six months ago.

Closing

This system isn't designed to be fast.

It's designed to be repeatable.

Because the goal isn't to have one good week. It's to run the same process every week — long enough for the balance to actually move.

At $439 per month in interest, every week the system runs is a week that cost is working against a shrinking balance instead of a static one.

Keep Reading

If you're new here, this baseline connects to the full system: