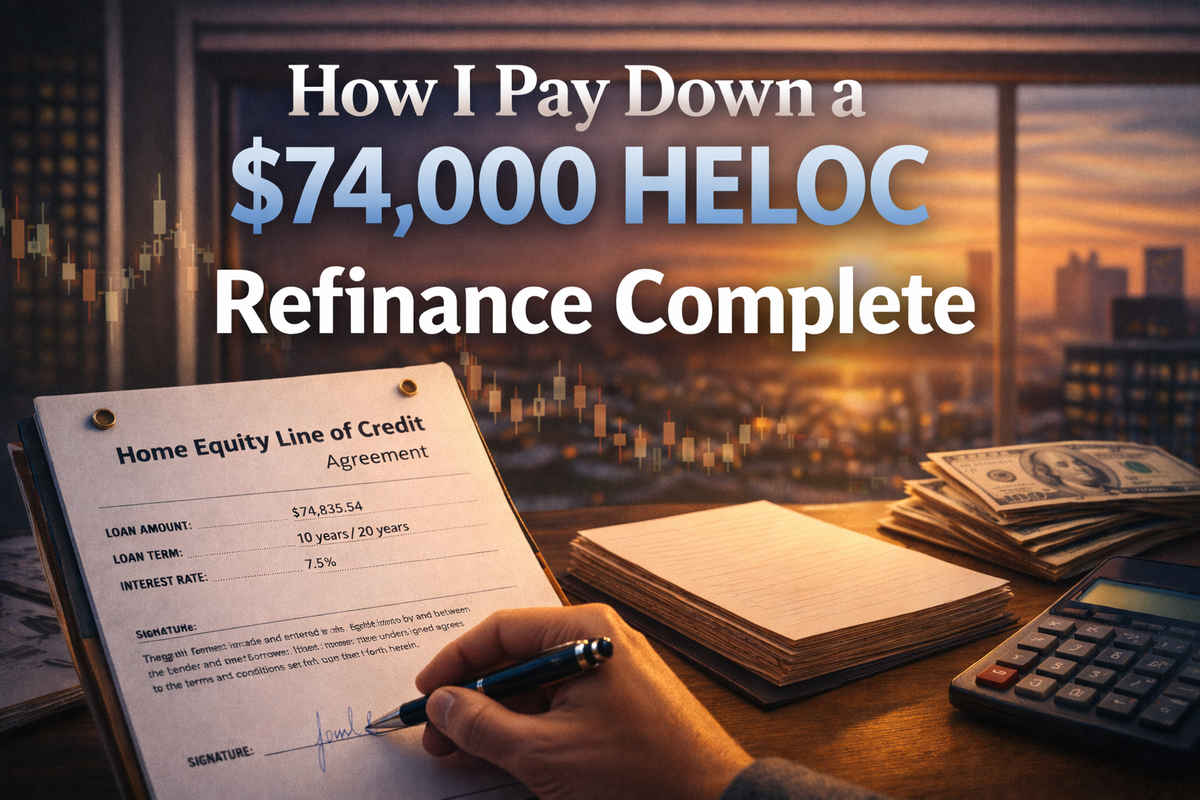

I Just Refinanced My HELOC — Here's What Changed (And What Didn't)

The refinance I planned from the beginning finally happened. The numbers changed. The system didn't.

On April 15, 2026, I closed on a new HELOC with the same credit union. The old balance was paid off at $74,835.54. The new HELOC opened at that same amount — then I immediately made a $435 principal payment, bringing the balance to $74,400.

If you've been following along, this wasn't a surprise.

Back in The System (v1), I wrote this out directly:

The plan is: pay down the current balance, improve how I use the credit line, eventually refinance into a new HELOC with a fresh draw period and higher limit.

That refinance just happened.

Here's what actually changed — and what it means going forward.

What Changed

Why Now — The Draw Period and Renovations

The original HELOC's draw period was approaching its end. Once a HELOC exits the draw period, it transitions into repayment — you lose the ability to borrow against the line, and the payment structure typically converts to a fully amortizing payment, which is usually higher.

That constraint was real. Phase 1 renovations — replacement windows, stucco, siding, and exterior paint — are planned for late summer. Waiting until after the draw period ended would have meant refinancing during the middle of renovation work or being locked out of the line entirely when the draws needed to happen.

With the refinance, that clock resets. The draw period is extended. The flexibility the HELOC is supposed to provide — as a tool, not just a debt — is restored before the work begins.

That was the point.

The Draw Period Is Reset

The new HELOC has a fresh 10-year draw period. The ability to access the line when Phase 1 work starts is no longer a question. The system can absorb the draws, the renovations move forward on schedule, and paydown resumes once the work is complete.

The Credit Limit Is Much Higher

The new credit limit is $365,000.

That's a significant increase from the original HELOC. This doesn't mean the balance is going up — it means the available credit reflects what the property can actually support. The limit is structural. How much of it gets used, and for what, is still governed by the same rules the system already has in place:

- No draws without a defined purpose

- Any new draw must be something the system can absorb

- Phase 1 renovations are already categorized and planned for late summer

The higher limit doesn't change the plan. It just removes a ceiling that didn't need to be there.

The Interest Rate Went Up

This is the tradeoff, and it's worth being direct about it.

The old rate was 7.115%. The new rate is 7.5%.

That's an increase of 0.385%.

On a $74,400 balance, the math looks like this:

- Old monthly interest: ~$443

- New monthly interest: ~$465

- Difference: ~$22/month more, or about $264/year

That's the cost of the refinance in real terms. There were no points, no large upfront costs — but the ongoing rate is higher, and that's the number that matters.

If the balance stays flat for a year, that's the full $264. But the system is designed to bring the balance down — so the actual cost of the higher rate decreases every month as principal drops. The $264 annual figure assumes a static balance. The balance isn't static.

Is that worth it for an extended draw period and a reset credit line?

For this situation, yes. The draw period constraint was real. The renovations are coming. And carrying a higher rate for a year while the balance is actively coming down costs less than being locked out of the draw period before the work is done.

But it's still a cost, and it shows up every month.

The System Keeps Running

The 6-step weekly cycle still applies:

- Observe the cash position

- Confirm obligations are covered

- Run the HELOC layer (minimum + opportunistic paydown)

- Run the options engine

- Layer in additional income

- Classify the week

The HELOC account changed. The process didn't. That's the point of building a system that works regardless of which account it's applied to.

The Options Engine Target

The $50,000 threshold stands.

The options account needs to reach a level where the premium it generates can cover the HELOC minimum payment. The minimum will be slightly higher now — the rate increased, so the interest component of every payment is a bit larger. But the target doesn't change. The engine still needs to prove it can carry the minimum before any premium gets redirected.

The Rules

The same rules from the beginning still apply:

- No new draws without a defined purpose

- Credit cards are timing tools — not long-term debt

- Extra principal payments come from actual surplus

- Everything gets tracked and shared publicly

The new HELOC doesn't reset the discipline. It restores the flexibility — under the same constraints.

What Needs to Happen Before May 25

The automated minimum payment needs to be confirmed or relinked to the new account. A missed payment on a newly opened line isn't acceptable — this gets handled before the first due date on May 25.

What Gets Updated Going Forward

The baseline numbers. The starting balance for the new HELOC is $74,400 at 7.5%. The estimated monthly interest is now ~$465, not ~$443. Everything going forward gets measured from this point.

The weekly classification context. The first few weeks on the new HELOC are effectively a reset. The balance is close to where it was. The system is the same. But the account is new, the rate is slightly higher, and any progress from here is being measured against a fresh starting point.

The Tradeoffs Were Clear

The rate went up. That's real money — $264 more per year than before.

But the draw period was going to end. The renovations are coming. And having the system already in place before the refinance happened means this isn't starting from scratch — it's continuing the same process with updated inputs.

The balance didn't balloon. The draw period is extended. The credit limit reflects the actual asset. The system keeps running.

That's what a planned refinance is supposed to look like.

What's Next

The first due date on the new HELOC is May 25, 2026.

Between now and then:

- Confirm the automated minimum payment is linked to the new account

- Continue the weekly cycle on the updated balance

- Keep the options engine on track toward $50K

- Get Phase 1 renovation quotes finalized so draw timing is clear before summer

Weekly updates will continue as usual — same format, same process, updated numbers.

If you're new here, start with the strategy or how the system works.